Form 1099: 1099-NEC, 1099-K, and 1099-MISC

These different 1099 forms are used to report non-employment income on 1040 tax returns. Freelancers, independent contractors, other self-employed and gig workers, NIL athletes, landlords, individuals earning dividends from stocks, and anyone else receiving non-employment income should receive a 1099 form by January 31 for the previous year’s income.

Be aware that even if you did not receive a form but earned 1099 income, you are still responsible for including it on your return.

1099-NEC

1099-NECs report payments of $600 or more to non-employees for services rendered. Businesses such as sole proprietors, partnerships, and corporations must issue a 1099-NEC form to entities that provided $600 or more in services.

1099-K

Individuals or companies that accept payments via debit card, credit card, or third-party payment networks like Venmo and PayPal are required by the IRS to file 1099-Ks if the individual or company has accumulated over 200 transactions exceeding $20,000 for tax year 2023. In 2024, the IRS plans to lower this amount to $5,000.

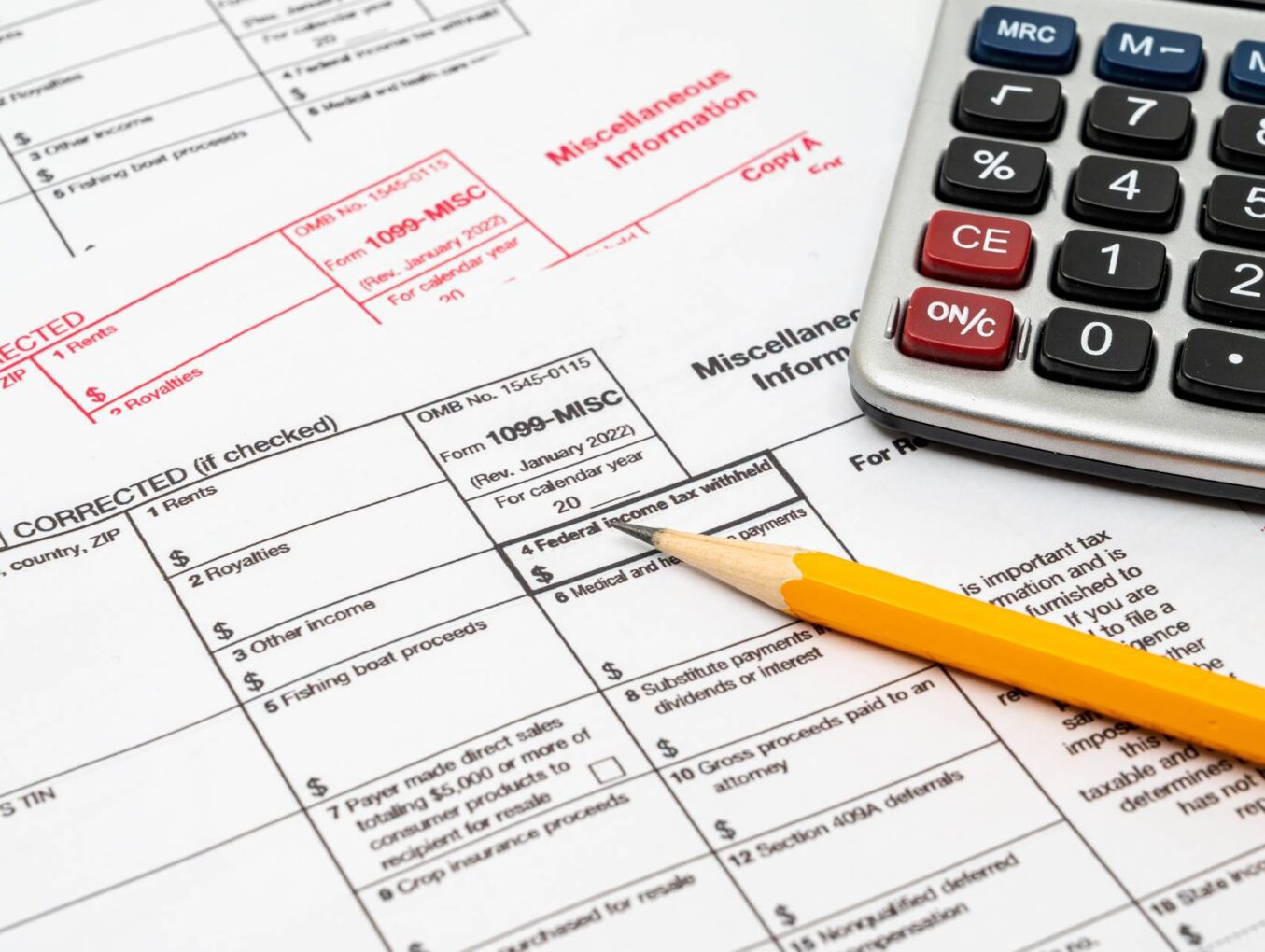

1099-MISC

1099-MISCs report various income such as rent, royalties, medical care, and other miscellaneous payments received.

Form 1040-ES: Estimated Tax for Individuals

Form 1040-ES is used for paying estimated taxes on income without withholding. Self-employment income, rent, dividends, interest, and money received from selling assets are types of non-employment income that require the filing of a 1040-ES with the IRS.

Individuals can estimate yearly income and calculate expected taxes by applying the appropriate tax rates and deductions to estimated income. Form 1040-ES also provides worksheets to help taxpayers determine quarterly estimated tax payments.

These payments are typically due on April 15, June 15, September 15, and January 15 (of the following year). However, if any of these quarterly tax payment dates fall on a weekend or holiday, the payment is due on the next business day.

Form 1040-ES helps individuals pay enough tax throughout the year so they will not be stuck with a large tax bill when they file in April.

Publication 505: Tax Withholding and Estimated Tax

Publication 505 for tax withholding and estimated tax provides instructions on how to calculate and manage federal income tax withholding and estimated tax payments throughout the year.

Topics covered in Publication 505 include how to calculate the correct amount of taxes to withhold from paychecks, Employee Withholding Certificates (EWC), instructions regarding estimated tax payments, and W-4s.

IRS 505 also addresses special situations that may affect tax withholding and estimated taxes, such as changes in marital status, additional income sources, tax credits, and deductions.

Taxpayers will find additional guidance concerning interest and penalties applied to overdue taxes and references to helpful IRS resources in publication 505.

Schedule C: Profit or Loss From Business (Form 1040 or 1040-SR)

Filed as part of a 1040 or 1040-SR, Schedule C for profit or loss from business is for single-member LLCs, sole proprietors, and self-employed individuals to report business income and expenses.

In addition to reporting income earned from selling services or goods, filers of Schedule C will find instructions for calculating net profits or losses and deducting certain business expenses, such as employee wages, rent, insurance, supplies, and even advertising costs.

Sole proprietors and single-member LLCs must file Schedule C if their business generates a gross income of $400 or more during the tax year.

If a business did not have a profit, it is still important to file Schedule C to report losses and to claim qualifying deductions.

Schedule SE: Self-Employment Tax (Form 1040 or 1040-SR)

Schedule SE determines the tax owed by self-employed individuals. Self-employment tax is Medicare and Social Security taxes for the self-employed (freelancers, gig workers, independent contractors, NIL athletes, etc.).

While employees have these taxes withheld from their paychecks, self-employed individuals must pay the full 15.3% tax themselves.

With Schedule SE, self-employed persons can calculate the self-employment tax for net earnings. Combining the 12.4% Social Security tax and 2.9% Medicare tax, self-employed individuals will owe 15.3% of net earnings for total self-employment taxes.

Need more help? You can start online by answering 6 simple questions.

6 Simple Questions. Free Evaluation.